Lecture 11: Foreign Exchange — Rates and Determination

Econ 2203 | International Trade and Policy in Agriculture

Nithin M

Department of Development Economics

2026-07-04

Foreign Exchange: Rates and Determination

How the rupee’s price against the dollar shapes India’s agricultural exports, food prices, and farmer incomes — and what economic theory tells us about why exchange rates move.

What is an Exchange Rate?

The nominal exchange rate is the price of one currency in terms of another.

\[e = \text{units of domestic currency per unit of foreign currency}\]

Direct quote (India convention): ₹ per USD — how many rupees to buy 1 dollar

Indirect quote: USD per ₹ — how many dollars 1 rupee buys (= 1/83.5 = $0.012)

India 2024: The RBI reference rate hovered near ₹83–84/USD throughout 2024. A software exporter invoicing $1M receives ₹83.5 crore at spot. A food importer buying $1M of edible oil pays ₹83.5 crore. The same rate creates winners and losers simultaneously.

Why forward rates matter for agri exporters: An Indian basmati exporter signing a 3-month USD contract today faces uncertainty — if INR appreciates by delivery, they receive fewer rupees. By selling USD forward at ₹84.2/$, they lock in their revenue. The forward premium (3.35%) reflects market expectations of INR depreciation.

Nominal vs Real Exchange Rate

The nominal rate tells us the currency price. The real rate tells us purchasing power competitiveness.

\[q = e \cdot \frac{P^*}{P}\]

where \(q\) = real exchange rate, \(e\) = nominal rate (₹/$), \(P^*\) = US price level, \(P\) = India price level.

Numerical example — Basmati Rice:

India price: ₹5,010/quintal; US equivalent: $60/quintal; \(e\) = ₹83.5/$

If India inflation pushes price to ₹5,600 with same nominal \(e\): \(q = 83.5 \times (60/5{,}600) = 0.894\) → INR real appreciation → Indian rice less competitive even though nominal rate unchanged

Why the real rate is what matters for trade competitiveness: India’s nominal exchange rate may be stable, but if domestic inflation outpaces foreign inflation, Indian goods become relatively expensive. Only a real depreciation — either a nominal depreciation or lower relative inflation — genuinely improves export competitiveness.

Real Effective Exchange Rate (REER): Trade-weighted average across all trading partners:

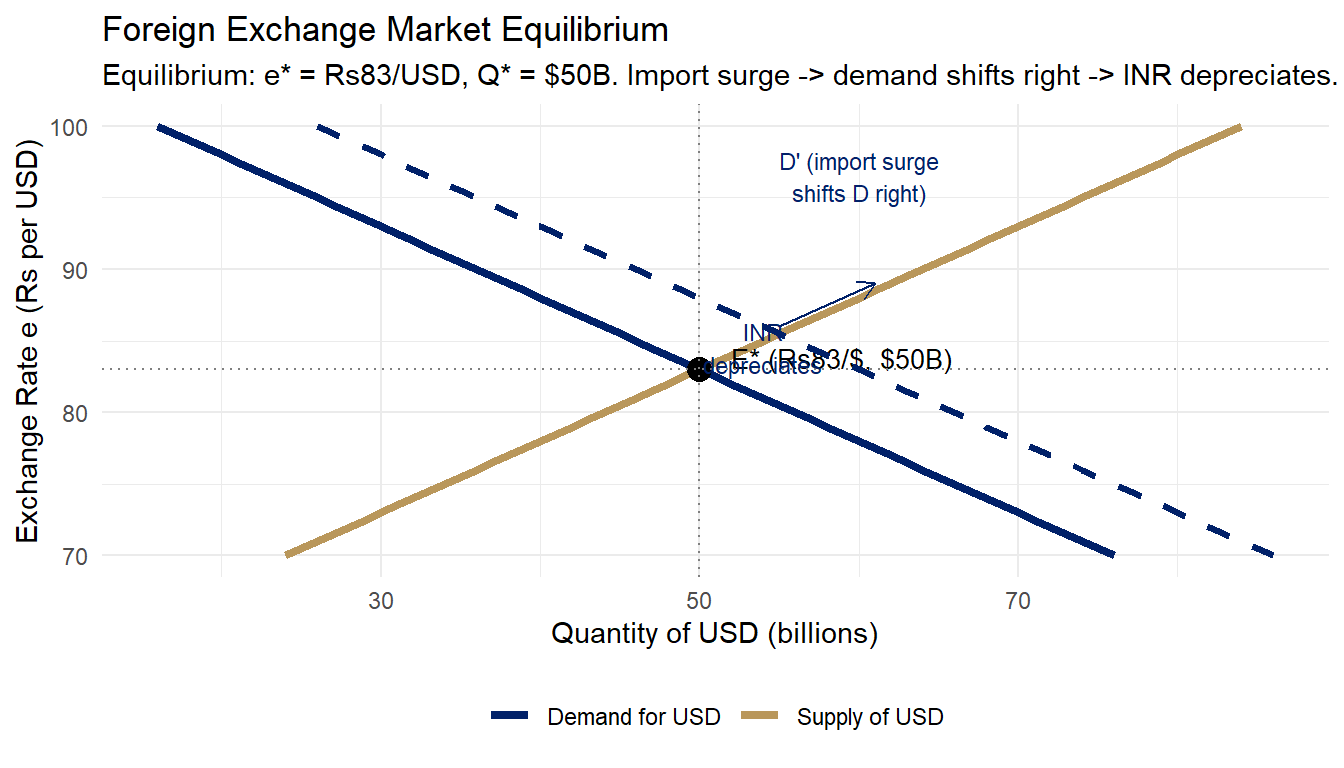

Demand function: As \(e\) rises (INR depreciates), imports become expensive → quantity of USD demanded falls.

\[Q_D = 216 - 2e\]

where \(e\) is ₹ per USD and \(Q\) is billions of USD. Downward-sloping demand curve.

Agricultural angle: India’s edible oil imports (~$14B/year) are the largest agricultural component of USD demand — palm oil from Indonesia/Malaysia, soybean oil from Argentina/Brazil, sunflower oil from Ukraine. A weaker rupee makes every litre more expensive.

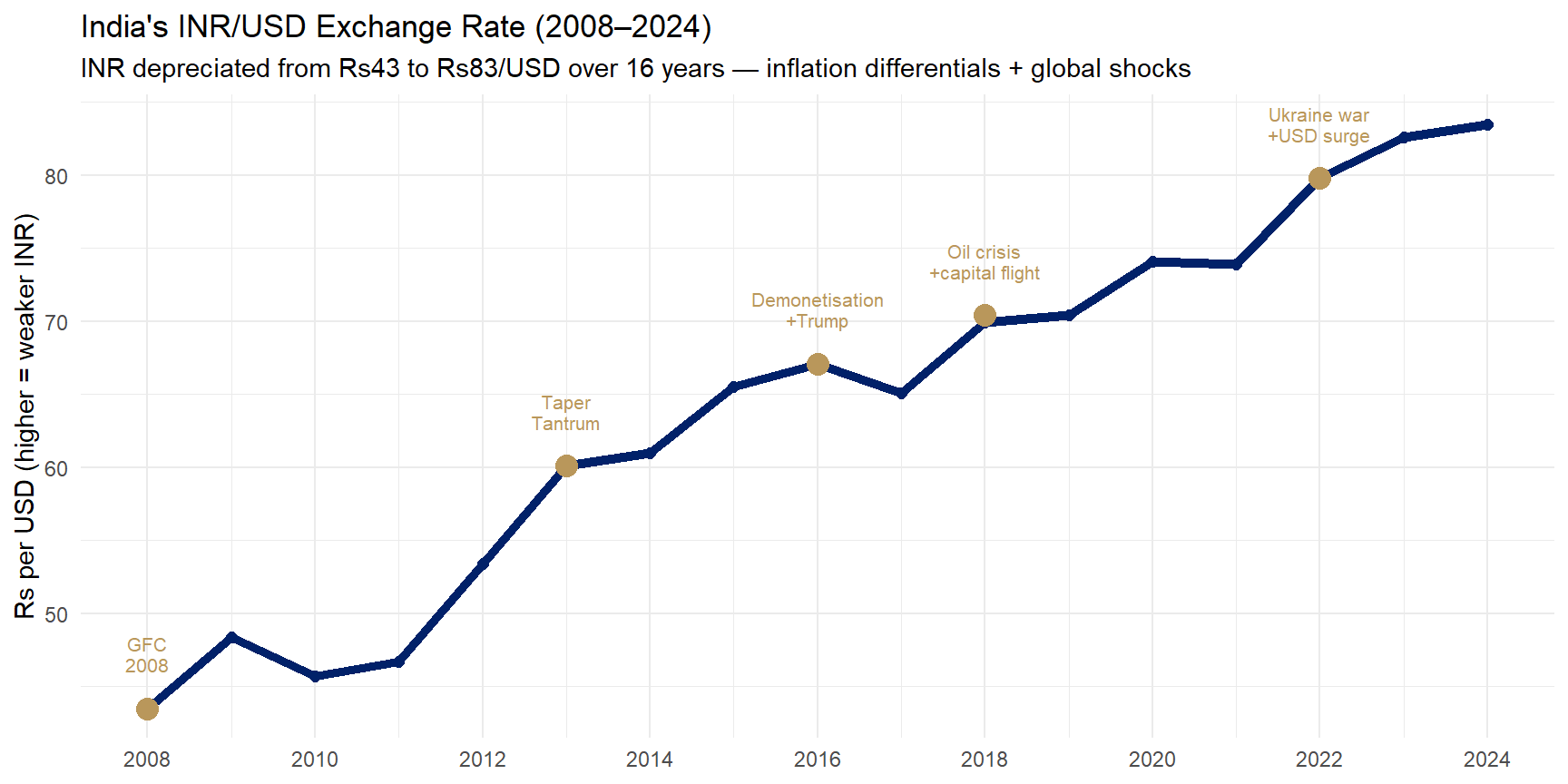

2018: Iran sanctions + crude oil surge. India’s $150B crude import bill inflated → INR hit ₹75.

2022 Ukraine: Sunflower oil import disruption + USD surge → edible oil crisis in India.

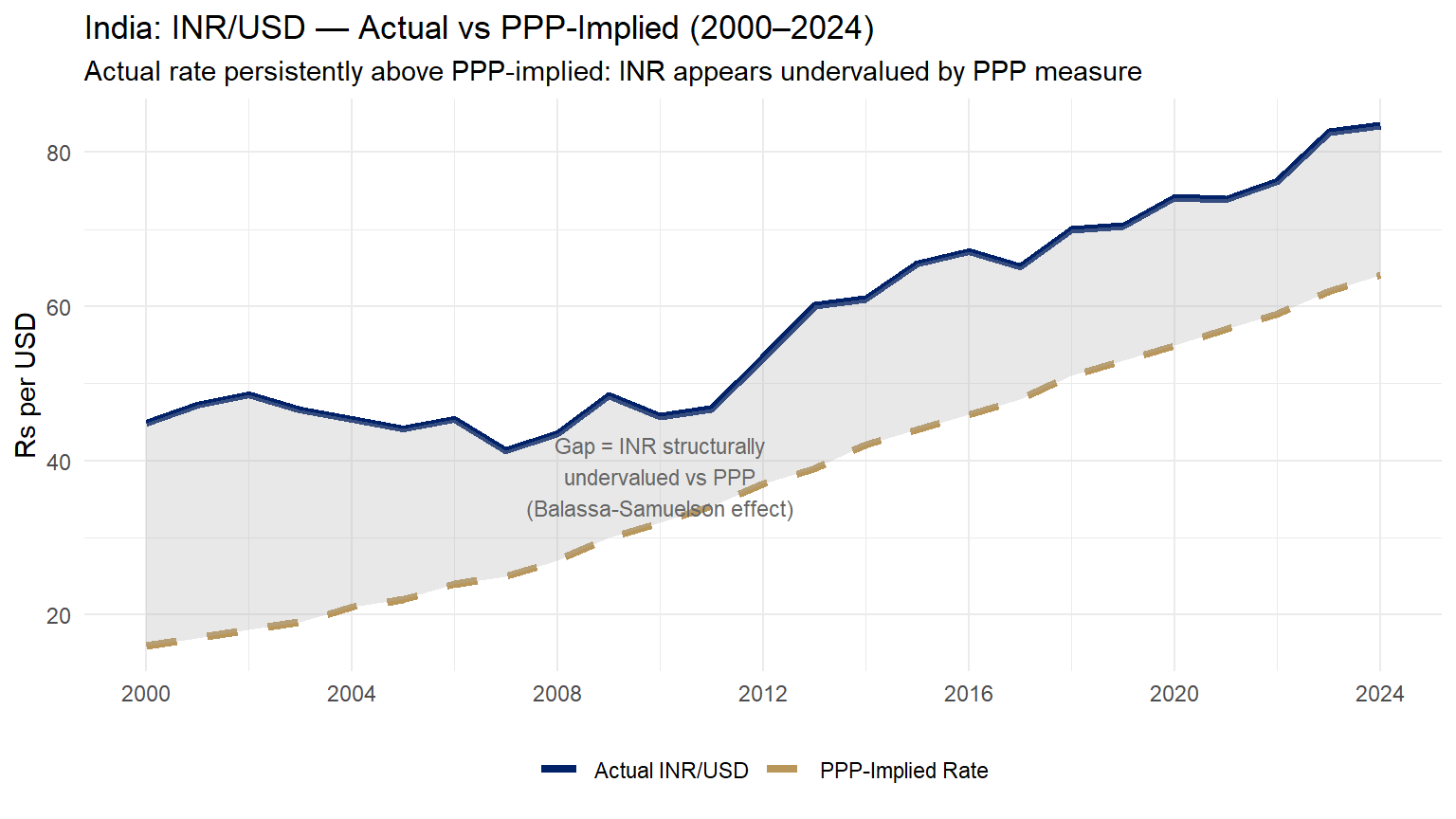

Purchasing Power Parity: Absolute PPP

Foundation — Law of One Price: In competitive markets with free trade, identical goods sell at the same price internationally (once converted at the exchange rate).

Absolute PPP: If a representative basket costs ₹4,175 in India and $50 in the USA:

\[e_{PPP} = \frac{P_{India}}{P_{USA}} = \frac{4175}{50} = ₹83.5 \text{ per USD}\]

Absolute PPP says: the exchange rate should equal the ratio of price levels. If the actual rate differs from PPP, there is a real misalignment.

Big Mac Index 2024 — Reality Check:

Item

India

USA

Big Mac price

₹259

$5.69

Implied PPP

₹259/\(5.69 = **₹45.5/\)**

—

Actual rate

₹83.5/$

—

Verdict

INR undervalued by ~45% vs PPP

—

This does not mean INR is “wrong” — it reflects real structural differences (Balassa-Samuelson effect, see Slide 13).

Relative PPP

Relative PPP: Exchange rates change in proportion to inflation differentials.

\[\% \Delta e \approx \pi_{India} - \pi_{USA}\]

Numerical example:

If India’s inflation \(\pi_{India} = 5\%\) and USA’s \(\pi_{USA} = 2\%\):

\[\% \Delta e = 5\% - 2\% = +3\% \Rightarrow \text{INR depreciates 3\% per year}\]

Long-run empirical test for India:

₹45/USD (2000) → ₹83.5/USD (2024): 85.6% depreciation over 24 years → ~3.5% per year

India avg CPI inflation (2000–2024): ~5.5%; US avg: ~2.2% → differential ≈ 3.3%

✓ Broadly consistent with Relative PPP!

Agricultural implication: Relative PPP predicts that India’s ~3–4% annual INR depreciation roughly offsets the ~3% domestic cost inflation facing Indian farmers. This means Indian agri exports maintain their global price competitiveness in the long run — inflation at home is offset by depreciation in the exchange rate. Short-run deviations, however, create real competitive swings.

Figure 3: India: Actual Exchange Rate vs PPP-Implied Rate (INR/USD, 2000–2024) Source: RBI; World Bank, International Comparison Program (ICP).

Balassa-Samuelson Effect: Fast-growing economies (like India) have high productivity growth in tradables (IT, manufacturing) but not in non-tradables (haircuts, local food). This raises wages overall, making non-tradables expensive. PPP calculations using full CPI baskets therefore understate the “true” exchange rate for a developing economy — the gap between actual and PPP-implied is structurally expected, not a sign of manipulation.

Limitations of PPP

PPP is a powerful long-run benchmark but has important practical limitations:

Non-tradable goods — haircuts, education, land, local restaurants don’t arbitrage across borders. Their prices differ permanently.

Quality differences — a “Big Mac” in Tokyo ≠ a Big Mac in Delhi in quality perception.

Trade barriers — tariffs, quotas, and transport costs prevent price equalisation even for tradables.

Balassa-Samuelson effect — richer/faster-growing countries systematically have currencies above PPP because productivity gains in tradables spill over to raise wages in non-tradables.

Short-run irrelevance — capital flows, sentiment, and central bank intervention dominate short-run exchange rates. PPP explains long-run trends, not day-to-day movements.

Agricultural implication: Agricultural commodities — rice, wheat, cotton, edible oils, spices — ARE tradable goods. PPP-based analysis is therefore more applicable to food prices than to services prices. When the IMF/World Bank assess food affordability across countries, they use PPP-adjusted incomes. India’s apparent INR undervaluation by PPP helps explain why Indian agricultural exports are consistently price-competitive globally.

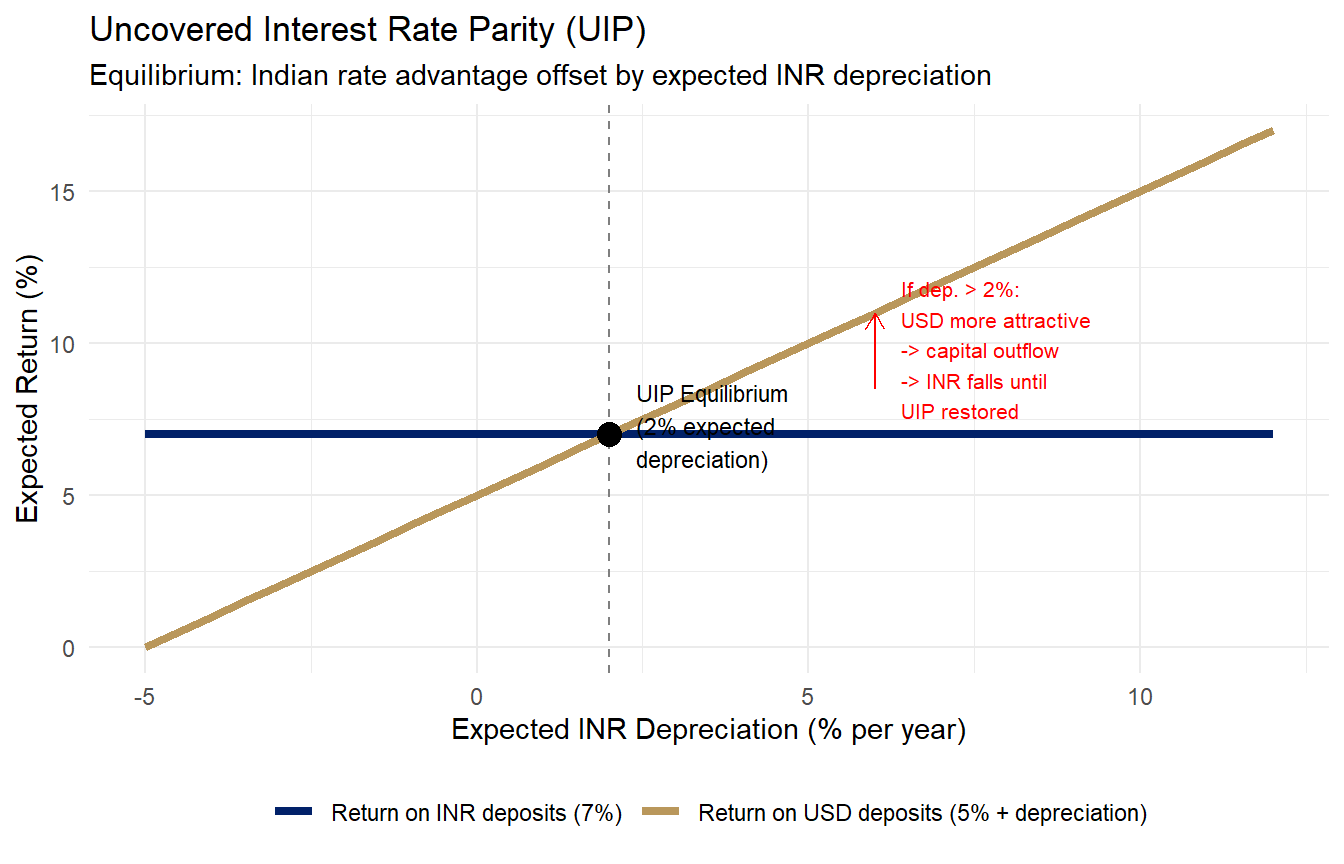

Interest Rate Parity: Uncovered IRP

Setup: An Indian investor has ₹1 crore to invest for 1 year. Two options:

INR bond earning \(i_{India} = 7\%\) → get ₹1.07 crore in 1 year

USD bond earning \(i_{USA} = 5\%\), but must convert ₹ to $ now and $ back to ₹ later

Uncovered Interest Rate Parity (UIP): In equilibrium, expected returns must be equal:

→ Market expects INR to depreciate 2% per year to equalise returns.

Interpretation: India’s higher interest rates do NOT simply attract unlimited capital inflows — because investors price in the expected currency depreciation. The interest rate advantage is exactly offset (in equilibrium) by the expected loss from holding a depreciating currency. This is why India cannot run 8% rates indefinitely without currency pressure.

Interest differential: \(i_{India}=6.5\%\), \(i_{USA}=5.3\%\) → \(\Delta i = 1.2\%\)

Gap (3.35% vs 1.2%) is explained by country risk premium on Indian sovereign debt.

Agri exporter hedging via CIP: A rice exporter expecting \(5M in 6 months sells USD forward at ₹84.2/\). CIP guarantees the forward rate is fairly priced relative to the interest differential — no “free money” from hedging, but the exporter eliminates revenue uncertainty. The forward premium (3.35%) is the cost of certainty.

RBI Intervention in the Forex Market

How RBI intervenes:

Preventing excessive depreciation: RBI sells USD from reserves → increases USD supply in market → reduces e (strengthens INR)

When RBI buys USD (injects ₹ into economy): 1. Buy USD → ₹ liquidity increases (inflationary) 2. Simultaneously sell government securities (G-secs) → absorbs ₹ back 3. Net effect: money supply neutral, but forex reserves increase

India’s forex reserve trajectory:

Year

Reserves

Import cover

1991

$1.2B

2 weeks (crisis)

2004

$113B

~12 months

2014

$304B

~8 months

2024

~$645B

~11 months

Sterilisation and agriculture:

When RBI sterilises USD purchases: - G-sec yields are kept from falling - Domestic interest rates remain higher - This keeps credit costs for agri sector elevated

RBI’s twin mandate — currency stability + price stability — creates a constant tension in agri credit markets.

India is NOT classified as a currency manipulator by the US Treasury — interventions are two-sided and RBI has intervened in both directions over 2022–2024.

Determinants Summary Table

Factor

Channel

Effect on e (₹/$)

INR Direction

India inflation ↑

PPP/competitiveness

e ↑

Depreciates

India growth ↑ → imports ↑

Current account

e ↑

Depreciates

FDI/FPI outflows ↑

Capital account

e ↑

Depreciates

Oil prices ↑ (India imports 85%)

Import demand

e ↑

Depreciates

US Fed raises rates

Carry trade reversal

e ↑

Depreciates

Remittances ↑

Capital inflows

e ↓

Appreciates

RBI raises repo rate

Capital inflows

e ↓

Appreciates

Export boom (rice, IT)

Current account

e ↓

Appreciates

Implications for Agricultural Trade

Depreciation (e ↑: ₹75→₹85) — Winners (Exporters):

🌾 Rice (~$10B/yr): world’s No.1 exporter; ~10.7% cheaper for importers

Market equilibrium:\(Q_D(e) = Q_S(e)\) determines \(e^*\); shifts from trade and capital flows move equilibrium. Solving: \(216-2e = -116+2e \Rightarrow e^* = 83\)

Real exchange rate\(q = e \cdot P^*/P\): only real depreciation — not just nominal — genuinely improves export competitiveness. REER is the trade-weighted measure RBI monitors.

Absolute PPP:\(e_{PPP} = P/P^*\); India’s actual rate >> PPP (Balassa-Samuelson); Relative PPP:\(\Delta e \approx \pi - \pi^*\) — ~3–4% annual INR depreciation predicted and observed over 2000–2024.

Interest Rate Parity (UIP):\(i_{India} - i_{USA} = (E^e - E)/E\); India’s higher rates are offset by expected depreciation — no free lunch from the interest differential.

Agriculture: depreciation boosts rice/cotton/spice exports; raises edible oil/fertiliser import costs — a constant policy tension that explains India’s oscillation between export bans and import duty waivers.

Next Lecture: Exchange Rate Systems and Open Economy Macroeconomics

Lecture 12 (July 11, 2026):

Forex Market — Exchange Rate Systems and Open Economy Macro

We will cover:

Fixed vs floating vs managed exchange rate systems

The Impossible Trinity (Mundell trilemma)

Mundell-Fleming model: IS-LM-BP

Fiscal and monetary policy effectiveness under different regimes

RBI’s managed float in practice

India’s forex reserves: from crisis to abundance

Forward market and currency hedging

Exchange rate pass-through to agricultural prices

Bridge from today:

Today we learned how the rupee rate is determined by supply/demand, PPP, and interest rate parity.

Next lecture we study:

What system India operates under

How government policy affects the exchange rate

How open-economy macroeconomics links monetary policy, fiscal policy, and the exchange rate

Reading: Salvatore Ch 14-15; Appleyard Ch 20-21

Appendix

Additional Resources

Further Reading

International Economics — Salvatore (Ch. 15-16)

International Economics — Appleyard & Field (Ch. 15-16)